Liability Insurance Needed

America’s guides and outfitters offer a wide array of experiences and activities. From guiding elk hunters on horseback in the Rockies, to picking up waterfowl hunters at a local motel for a day of shooting sea ducks in Maryland or even hosting whitetail hunters in their own home at the peak of the rut, guides and outfitters must be part hunter, part host and part business professional. Of course, large scale operations usually have a full staff of guides, sales people and business advisors to help make sure the company runs smoothly and makes a nice profit. On the other hand, a much larger percentage of outfitters are making do with a handful of friends and family helping when and where they can.

What if you don’t have a professional staff to assist you in the operational side of your business? Considering time spent scouting, hanging stands, building blinds, improving habitat, marketing your company, selling trips and trying to make family time, is it surprising that important business decisions are sometimes made without all the needed information? For example, what liability insurance coverage do I need, what does it all mean, when do I need it and where can I purchase it easily and affordably?

We are here to guide you to those answers and provide you (or should we say ‘outfit you’) with a few good options and all the answers you need to make the right choice for your business.

What is liability insurance and why do I need it?

Your business is quite literally based on you assuming responsibility for your guests and their safety. Hunting from tree stands, wading in a stream to fly fish or even feeding them meals your cook has specially prepared for them. These are all examples of why you need to protect your business assets against claims of negligence. Hunting and fishing produce some inherent dangers. Although much less than some would have you think.

However, when a guest pays a fee for the service you provide, you then become responsible for their safety and well-being. Proper liability coverage for your business will defend you against claims and even law suits against your business. Including things for injuries or damage to personal property resulting from your unintentional negligence.

Not only is having proper liability coverage the right business decision for you and your guests. But is required of you to have this type of insurance in many states. The requirements placed on guides and outfitters vary from state to state. The first step when preparing your business should always be to do your research and discover what the requirements are for the state(s) you will be guiding/outfitting.

Custom Policy vs Master Policy

As long as there has been insurance there has been insurance agents. Professional agents fill a needed role for business owners and can be an important part of any company, especially large-scale operations. A custom written policy may be your best option if you are insuring large amounts of equipment. Also livestock (horses), a lodge and other items and personnel. An agent will work with you to write different coverages. That are based on the value of your equipment and/or the costs of replacement.

In addition, your insurance package should include a liability policy. Which protect you from the items we mentioned above. This type of policy is written specifically for your business needs and can start on any date you choose. The drawback to a custom policy is that the agent who writes it needs to build in enough premium to pay himself. As well as his agency and the insurance carrier. Obviously, this will raise the cost of your insurance.

The master policy has gained tremendous popularity in recent years. As business owners recognized their risks and needs closely matched those of other businesses and/or groups. A master policy is simply a policy that has predetermined coverages, limits and usually a specific start and end date. What makes a master policy attractive is the comparatively low cost (in some cases, the savings can be dramatic) to a custom written policy.

Custom Policy vs Master Policy Continued

Here is a good analogy for comparing custom and master policies. Consider the two as suits you need for an upcoming event. You can buy a custom-tailored suit: the tailor will take all of your measurements. Then talk to you about which fabric you like and make your suit specifically to your stated needs. It will take him a few weeks to complete and you can bet it will cost a little more. The alternative is to buy a suit from a nice department store that is already made, that you can try on and that looks and feels good. You can walk out of the store with it and save a significant amount of money. Both do the job. Which is best for you and your business? That’s up to you.

Choosing a Master Policy

There are two things to remember when choosing a master policy. First, the date your coverage begins is already determined. Even if the policy started on July 1, you can still purchase your policy and have full coverage moving forward from the day following purchase. So, if you have guests that are traveling to hunt with you in Oct, you can purchase your liability coverage on a master policy once you are certain they are coming and have paid their deposit. You will have coverage on this policy until the following July 1, at which time you can renew or wait again until you are certain you will need coverage.

Another important factor to consider with a master policy is that you will receive full coverage. As stated on the declarations page and will not share those limits with any other policy holder. If the coverage limits set by the policy are agreeable and address your outfitting business needs. Then you will receive the very same coverage benefits afforded to you in a custom written policy but at a much better rate.

Currently, the American Hunting Lease Association (Guides and Outfitters Full Liability Coverage) offers guides and outfitters full liability insurance coverage online or by phone. The AHLA will even email your certificate of insurance to you the following business day.

Add Landowners or others as additional insureds.

Unless you are fortunate enough to own the land you are guiding hunters or fishermen on. It is then likely you have others that will require you to purchase hunting guide insurance. The ability to add others to your policy as an additional insured is key and cannot be left out.

Adding an additional insured simply means that the person, group or even government entity you are adding also has the same coverage you have purchased. In the event one of your guests becomes injured while in your care, but on their land, the policy you have purchased will also defend that landowner in the event of a lawsuit. Frankly, most landowners require this policy specifically for this reason and it makes sense. The most common arrangement guides and outfitters use to acquire hunting rights on private land is to lease access directly from the landowner. Listing each landowner as an additional insured on a liability policy will protect their assets. Also greatly enhance your chances of accessing their land.

If you guide or outfit on public ground, the state or federal governments will require you to add them as additional insureds AND prove it by supplying them with their own certificate of insurance listing them as an additional insured. For example, the Bureau of Land Management, US Fish and Wildlife Service, State Wildlife Management Areas and all State Depts of Natural Resources may require a certificate of insurance. Make sure your policy meets their specific requirements.

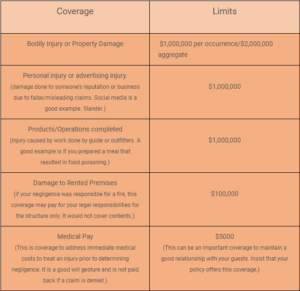

The coverages, what do they actually mean?

Remember, we are focused on liability coverage for your hunting guide business. Liability insurance is designed to protect you and your landowners. It is not medical insurance for you, your guides or even your guests. Simply stated, liability insurance never pays you. If you are found to be accidentally negligent and that negligence results in bodily injury, property damage or personal injury, then this coverage is activated. Below is a list of basic coverages and limits. The limits listed below are widely considered to be the industry standard for hunting or fishing guides insurance.

The Purchase Process. Does it have to be difficult?

Truthfully speaking, there just aren’t a lot of options for purchasing your insurance. The Hunting Guide Insurance industry has a tried and true method for marketing and selling insurance. Usually involving you operating on their schedule and at their pace. But it doesn’t have to be that was.

Typically, you will start your search for guides and outfitters insurance with a Google search to find an agency or organization that provides the type of coverage you are looking for. Once you find a few agencies that provide custom written policies. You can then call them direct. With the hope to speak to an agent or you can submit an online request for a quote and hope that someone will call you back. . . at their convenience. If the coverages and premiums are agreeable. Then you will likely be sent an application to fill out and return with your payment. Once payment is received, the insurance agency will call or email you back that your coverage is now in place. This may take up to 3 weeks to complete.

Hunting Guide Insurance Solutions

Thankfully this has begun to change as technology and consumer trust in internet purchasing grows. Organizations like the American Hunting Lease Association (AHLA Guides and Outfitters Master Program) have recognized the needs of guides and outfitters. Providing a process that respects their time. Purchasing your insurance online, through a secure website allows you to get an instant quote. Which lets complete applications and pay for your coverage at your convenience. Coverage begins the following day and your certificate of insurance will be emailed to you and your additional insureds as well. The real win for guides and outfitters that purchase liability insurance this way, is that they are able make sure clients or guests are on their way and can have full coverage in place before they arrive.

If you are a professional hunting or fishing guide shopping for liability insurance, there is a good chance you are doing so after putting in a full day already. Why wait for an insurance agency to take care of you during their business hours, when you can buy it yourself when, where and how it works best for you?

Key Takeaways

The one thing we know for sure is that all guides and outfitters are not created equal. Everyone has seen the large outfitters with beautiful lodges and large operations on outdoor television. However, the overwhelming majority of professional guides and outfitters in this country are smaller operations with limited resources and a different set of needs. Every business should do their best to research and determine the which insurance program is best for them. With liability insurance being one of the most important things you can get for your business.

Leave A Comment